Luc Lendrum, GHG and Climate Solutions Expert

Got questions? Register now for our webinar on December 8, 12:00 ET, and learn more about the Clean Fuels Regulation. Come and chat with our experts!

Canada’s Clean Fuel Regulations (CFR) came into effect on July 1, 2023. These regulations impose a reduction in the carbon intensity (CI) of transportation fuels of 15% below 2016 levels by 2030. The regulations create a market in compliance credits, providing flexibility for fuel distributors and minimizing the total cost to Canadian society of these emissions reductions. While modelled on similar Low Carbon Fuel Standards in California, Oregon, British-Columbia, and Europe, the CFR includes unique characteristics. One such aspect that has received little attention to date is the partial inclusion of gaseous fuels. The legislation was originally targeted to apply to all fossil fuels in Canada, divided into solid, liquid, and gaseous classes. The solid- and gaseous-class obligations were dropped from the final text of the regulation, however the possibility to generate credits in the gaseous class remains.

NEL-i’s services were retained by the Régie de l’énergie du Québec (Quebec Energy Board) to explain trends in the CFR credit market and to project future price evolution and market dynamics. The key findings reported below came to light in the context of this mandate, making them part of the public record.

Before addressing the effects of this inclusion, a summary of the three categories under which compliance credits can be created:

- Compliance Category 1: Actions throughout the lifecycle of a liquid fossil fuel that reduce its CI through GHG emission reduction projects

- Example: Carbon capture and storage at the refinery

- Compliance Category 2: Supplying low CI fuels

- Example: Blending ethanol in gasoline

- Compliance Category 3: End-use fuel switching in transportation

- Example: Reduction of gasoline/diesel demand from a switch to electric vehicles

The obligations of fuel suppliers (the “Primary Suppliers”, as referred to in the regulation) are measured in tonnes of carbon dioxide equivalent (t CO2e), and the CFR provides quantification methodologies to determine the credits that can be issued under each of these three categories. Fuel suppliers then use these credits to offset the deficits incurred from exceeding the CI limit, thereby meeting their obligations. The structure of this program ensures that emissions reductions are achieved in a cost-effective manner by penalizing emitters in proportion to their exceedance of emissions limits, while channeling funds to lower-carbon fuel producers in proportion to the “cleanliness” of their alternative.

While only liquid class (i.e. gasoline and diesel) suppliers are obliged to lower the carbon intensity of their fuels, up to 10% of their obligation can be met with gaseous class credits, those issued from the production of renewable natural gas (RNG), renewable propane, and hydrogen not used in transportation. The two broad effects of this inclusion are, first, to ease the pressure on liquid fuel suppliers by increasing credit supply, and second, to provide an additional revenue source to RNG and renewable propane producers.

Credit Supply and Demand According to ECCC

Upon publication of the CFR, Environment and Climate Change Canada (ECCC) provided a Regulatory Impact Analysis Statement, where they sought to project the effects of these regulations on Canadian society. Part of their analysis was the estimation of the supply and demand of credits from inception through 2040. Credit supply was modeled according to the “cost of credit creation”, that is, the cost to reduce emissions by 1 ton of CO2e by each of the possible pathways. A fundamental assumption underlying this approach is that the market will find equilibrium between supply and demand at the lowest total cost. Therefore, a pathway with a higher cost of creation will only begin to produce credits when all cheaper pathways have been used to their greatest possible extent. While this assumption is at best approximate, the goal is to produce a useful model rather than a perfect one.

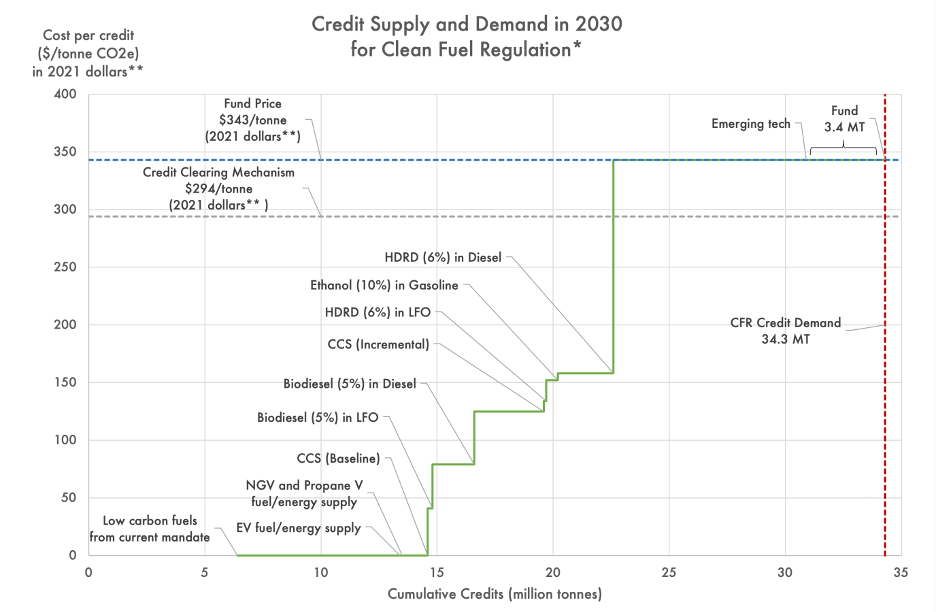

Here, in a graphic created by Grant Bishop based on ECCC’s analysis, we see the projected relationship between credit supply and demand in the year 2030. Almost 15 million “baseline” credits will be created at no cost – the credit-generating activities would have happened even in the absence of the CFR. To satisfy the remaining credit demand (represented by the red, vertical line), each progressively more expensive pathway comes online until its credit creation potential has been exhausted. The addition of these pathways brings supply to approximately 23 million credits. Ten percent of total obligations may be covered via contribution to a registered emission-reduction funding program (Compliance Fund) at $350/credit (2022 dollars), and any remaining demand is assumed to be fulfilled by technologies which are not yet economically viable, but are expected to become so due to this regulation (Emerging Technology). ECCC’s model assumes a price of $350/credit for this pathway, although the actual cost of creation from these emerging technologies may well be even higher. Since liquid class credits are fungible, it could be assumed in a perfectly efficient market that credits would transact at or above the marginal cost of creation. Due to illiquidity and information asymmetry, we relax that assumption to the expectation that credits will transact at or above their respective marginal costs of creation.

This approach to analysing the equilibrium between supply and demand is robust and uses the best data currently available, however, ECCC’s analysis did not consider the effect of gaseous class credits. Recall that each fuel supplier can meet 10% of its obligation using credits created in the gaseous class.

The Role of Renewable Natural Gas (RNG)

The production of RNG in North America has more than doubled since 2019, motivated largely by low-carbon fuels mandates in the transportation sector. It is set to double again by 2030, encouraged by government mandates and businesses substituting RNG for natural gas in order to reduce their GHG emissions and hence their carbon taxes. Since most of this RNG would have been produced even in the absence of the CFR, we can consider the cost of creation of these gaseous class credits to be $0. The other question to address before including gaseous class credits in our analysis is whether enough of these credits will be created to meet the limit of 10% of compliance obligations.

To evaluate this possibility, we considered the volumes of RNG projected to be supplied by Fortis BC, Enbridge, and Énergir, Canada’s three largest natural gas suppliers from now to 2030 (as reported in evidence submitted by Énergir to the Quebec Energy board). We found that these volumes alone would saturate the demand for gaseous class credits if the average carbon intensity of these fuels is less than (i.e. better than) -5 g CO2e/MJ. Considering that the carbon intensity of RNG supplied to California’s LCFS program is -110 g CO2e/MJ, the saturation of gaseous class credit demand becomes a near certainty. Note that this “near certainty” of saturation holds only so long as the market value of gaseous class credits justifies the administrative burden of voluntary participation in the CFR and low-carbon Canadian RNG is not redirected for export to a jurisdiction where it would have greater value.

Credit Supply and Demand According to NEL-i

In our modelling approach, in addition to considering the contribution of gaseous class credits to the overall supply, we diverged in one other respect from ECCC, by increasing the cost of credit creation from “emerging technologies”. ECCC’s value of $350 per credit was selected to be equal to the cost of the Compliance Fund, as a rigorous evaluation of the costs of emerging technologies would be a contradiction in terms – these technologies are not yet commercially viable. Breakthroughs will be required, and the surest way to encourage these breakthroughs is commercial incentive. For the purposes of our modeling, we have set the cost of creation at an arbitrary premium of $26 to the cost of the compliance fund. This premium represents the inherent uncertainty of emerging technologies, and fuel suppliers’ ensuing preference for the certainty of the compliance fund.

All other ECCC data was maintained, including their projections for declining liquid fuel demand and increasing electric vehicle uptake. For commentary on these projections, see Grant Bishop’s analysis.

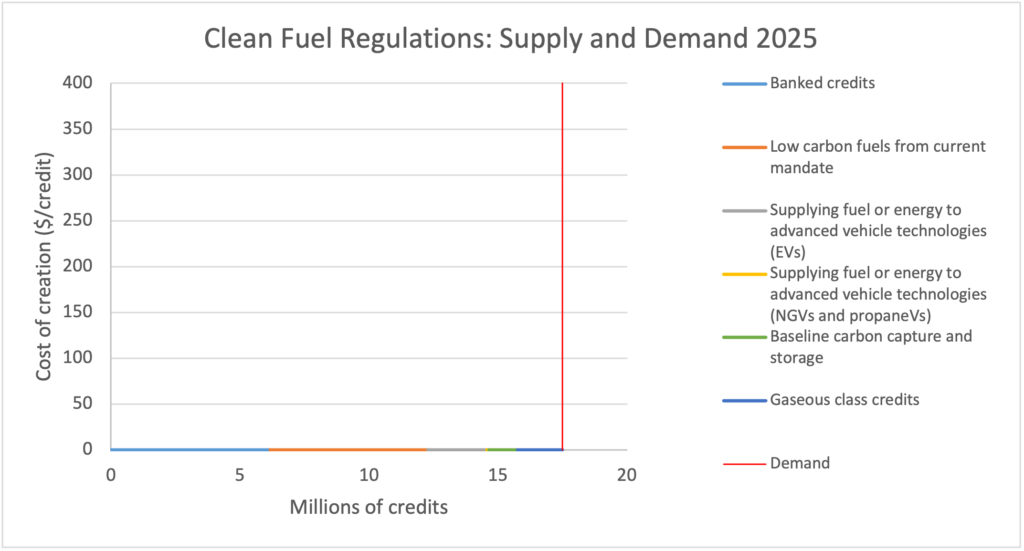

Supply-Demand Dynamics Until 2025

Until the end of the 2025 compliance period, fuel suppliers will be able to meet their obligations using only baseline credits – those resulting from activities independent of the CFR, as represented by the horizontal line at the $0 level of Figure 2. The colours of the line segments represent the pathways by which the credits are created: banked credits from prior years and low-carbon fuels from existing mandates fulfill approximately 1/3 of the demand each, with electric vehicles and the gaseous class fulfilling 12.5 and 10% respectively.

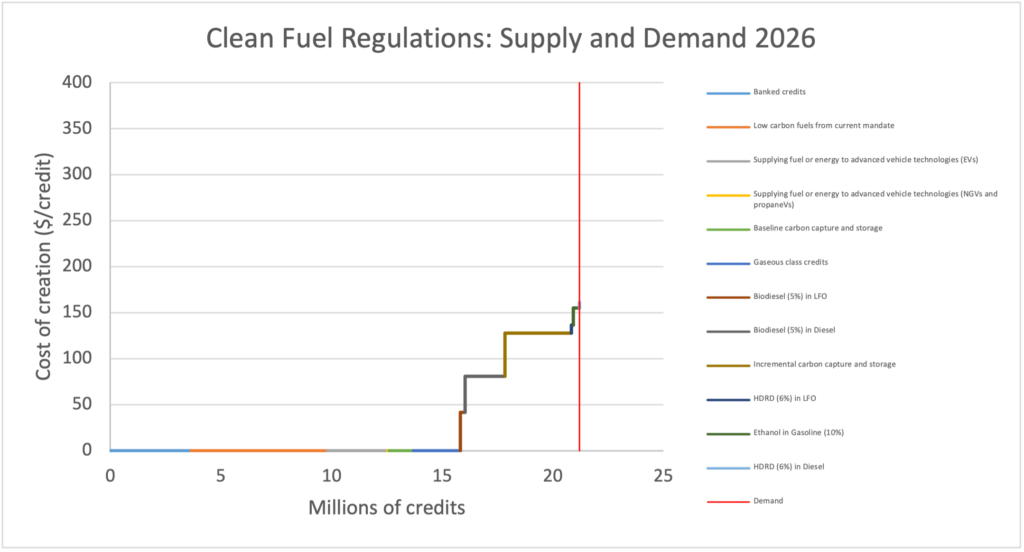

Supply-Demand Dynamics in 2026

2026 is the first year in which “incremental” (i.e. non-baseline) credit creation will be required. This is the year when banked credits are set to run out and six new pathways will be required to meet demand. To bring these pathways online will require planning and capital expenditure. The incentive for this incremental credit creation is that the alternative would be to purchase credits from the compliance fund at a cost of $350, well above both the average and marginal costs of creation for this year of $28 and $155, respectively.

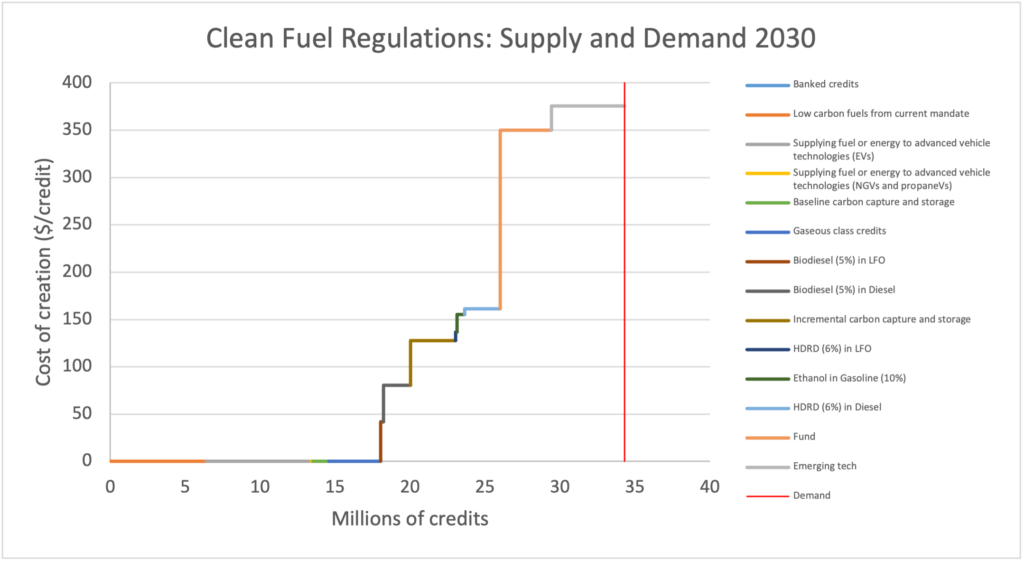

Supply-Demand Dynamics From 2027 – 2035

As of 2027, the compliance fund will be required for its full 10% maximum contribution, in addition to over a million credits from emerging technologies. These two categories will continue to be required until 2036 when the combination of reduced liquid fuel demand and greater market penetration of electric vehicles will lead to a gradual decline in the marginal cost of creation. Figure 4 shows a snapshot of the year 2030, which is representative of this period and can be contrasted with Figure 1 (ECCC’s analysis of the same year). We note that while emerging technology remains the marginal credit creation pathway, its contribution, relative to Figure 1, is reduced by 3.4 million credits, equivalent to the demand for gaseous class credits that year

Supply-Demand Dynamics From 2036 – 2040

As of 2036, due to a continuation of the forecasted reduction in liquid fuel demand and increase in electric vehicle penetration, emerging technology credits will no longer be required to satisfy demand. The maximum 10% contribution of the compliance fund will no longer be required, though its use will not disappear entirely until 2040. By that year, the marginal cost of credit creation is projected to fall to $161, with an average cost of $30.

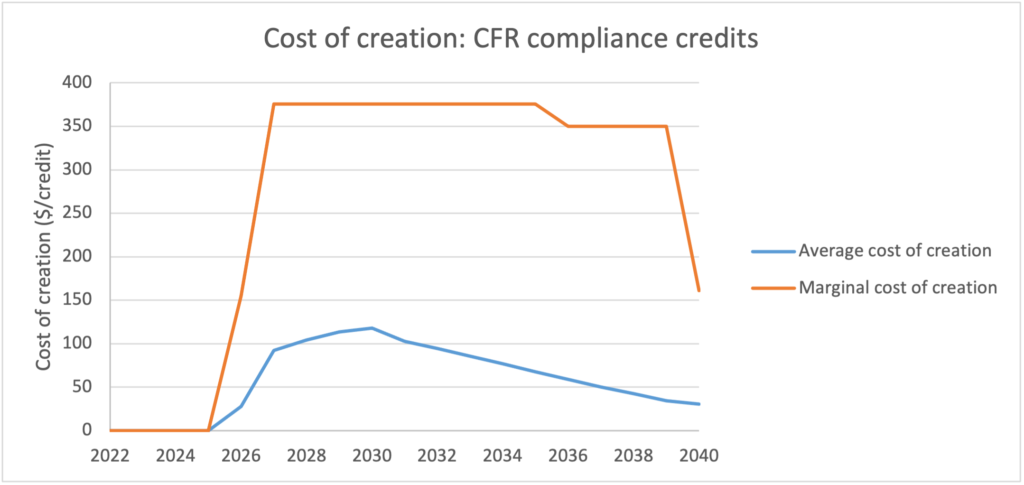

Average and Marginal Costs of Credit Creation

Figure 6 shows the evolution until 2040 of the average and marginal costs of creation. The differential between these values, stretching beyond $300 per credit in 2035 is indicative of the attractive margins available to low-cost credit producers. These margins will act as a powerful incentive for investment in clean fuel production capacity, for both primary suppliers and voluntary participants. Recall that these prices refer to liquid class credits; due to the likely saturation of the gaseous class credit demand, these credits should trade at a yet-to-be-determined discount to their liquid class counterparts.

As a ballpark estimate, our expectation is that the average transaction price of liquid class credits should fall between the average and marginal costs of credit creation in a given period.

Conclusion

The inclusion of the gaseous class in the supply modeling of the CFR credit market makes a significant difference, adding 10% to total supply. The primary effect of this inclusion is flexibility for primary suppliers in meeting their compliance obligations. A secondary effect is a supplementary incentive to production in Canada’s nascent RNG industry. While falling outside the strict scope of the regulation (i.e. transportation fuels), the inclusion of the gaseous class would seem to belong to the most favourable category of political compromise, those that keep costs low and producers happy, without undermining the policy’s central thrust.

The CFR is a well-designed piece of legislation in that it appears poised to accomplish its objectives of reducing GHG emissions from transportation in a cost-effective manner. While it has been broadly accepted by fuel suppliers, it is attracting unwelcome political attention, notably due to pre-emptive price hikes in New Brunswick and outright hostility from the leadership of the federal Conservative Party. Additionally, as Alberta’s government threatens to challenge the constitutionality of the proposed federal Clean Electricity Regulations, it must be noted that the CFR operates under the same legal framework and could get drawn into the same fight.

The downside of this political uncertainty is that it can give pause to companies considering investments in clean fuel production. Clarity from Canada’s political leadership would serve the interests of all parties. In the meantime, however, this enhances the opportunity available to baseline and “semi-incremental” clean fuel producers whose business case is not wholly reliant on the CFR. While others wait on the sidelines, these agile companies can reap the benefits.

Recent Comments